An IRA or individual retirement account or a plan, provided by various financial institutions. It provides tax benefits for retirement savings to the US residents. They are the powerful resources which help in reaching the aims of retirement savings. Sometimes regarded as “Individual Retirement Arrangements”, they consist of a series of financial products such as bonds, stocks or mutual funds. However, a self-directed IRA allows investors to obtain all of the investment decisions for their account provides access to a different series of investments like private placements, real estate, and tax liens.

Types of IRA

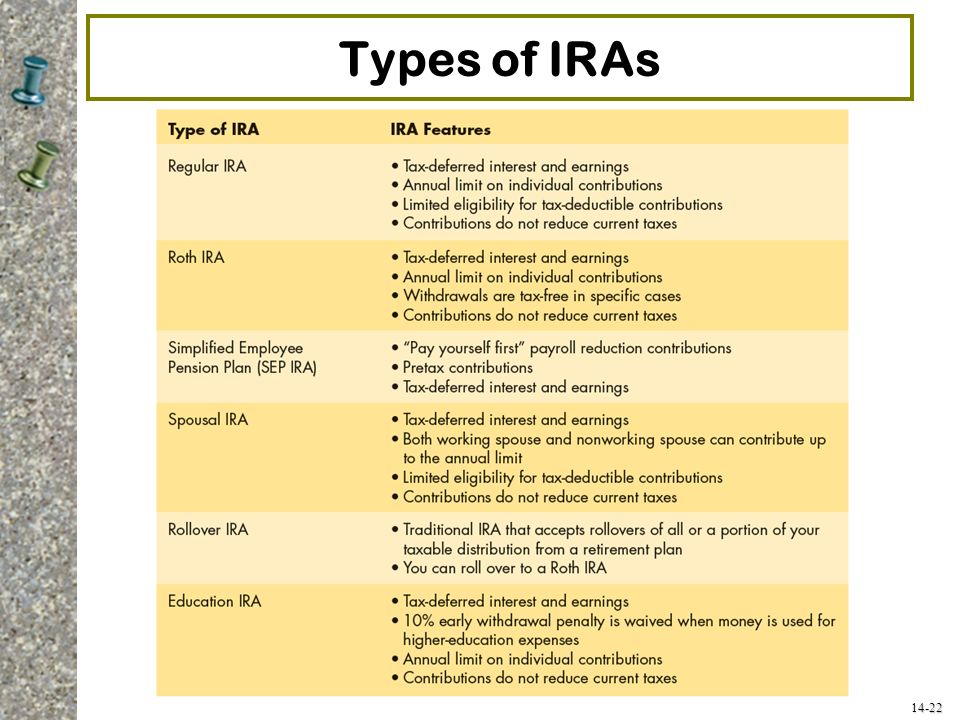

An IRA is a tool for investments where individuals use to allocate funds for retirement savings. There and several types of IRAs with different advantages. These are listed as below:

Traditional IRA Contributions to these are generally deducted on the tax returns. So, transactions and earnings can probably grow and not imply tax-deferred until the amount is withdrawn at the retirement. As of 2018, individual contributions annually to traditional IRAs should not exceed $5,500 in most of the cases. If the age limit is 50 plus then they can pay up to $6,500 annually utilizing catch-up contributions.

Roth IRA They are generally not tax-deductible, but qualified allowances are tax-free. This means that for any contributions to a Roth IRA is after-tax dollars, but as there is growth in the account, then there are no taxes on investment gains. At the retirement age, the withdrawals from the account are income tax-free.

SEP IRAs, Self-employed individuals, such as small-business owners, freelancers, independent contractors can obtain SEP (Simplified employee pension) IRAs. In regards to taxation rules, it is the same as the traditional IRA. However, in 2018, SEP contributions are restricted to 25% of compensation or $5,000 whichever is less. Entrepreneurs who obtain a SEP IRA for their businesses employees can subtract the contributions from their business income and secure a lower tax on that interest.

Spousal IRA, a type of individual retirement plan which supports a working spouse to pay for a non-working spouse’s retirement benefits. This creates an exemption to the procurement that an individual must have received income to contribute for IRA. However, the working partner’s income must exceed or equal the entire IRA contributions given on account of both spouses.

Rollover IRA provides employers a challenge of rolling funds from one into the other plans. In traditional IRAs, they don’t have the facility to roll back, as it is unidirectional. So, Rollover IRAs provides moving eligible assets from such an employer-sponsored plan like 401(k) or 403(b), into an IRA.

Education IRA also called as Coverdell Education Savings Account-ESA, since it is not an IRA. It is just a savings account which brings the tax saving advantages which are in line with IRA. An Education IRA is merely a tax-beneficial investment helpful for higher education.

Investing in IRA

People should start their investment as soon as they land into their first job. Many financial managers consider investing up to 85% of pre-retirement earnings in retirement. Anyhow, an employer-sponsored plan like 401(k) will not be enough to save the proceeds one needs.

Fortunately one can invest to both an IRA or 401(k). There is always a need to supplement the current earnings in the employer-sponsored savings plan. Always make a way for a potential and more extensive range of investment options. Having said that, IRAs can be opened through many financial institutions either through online or in person. Financial institutions include brokerage firms, local banks, mutual fund firms, and credit unions.

Conclusion

Without concerning about the age, which is never too late to start investing for retirement. But to accumulate a sizable income, there is a need to invest and help that income to grow. This is where an IRA comes conveniently. Investing in an IRA gives plenty of advantages which are tax-deductible up to IRS restrictions. It also provides a room for investing in an IRA that can decrease annual tax bill. However, an individual is restricted to withdraw the amount before 59 years there is always a privilege of paying for certain expenses. Having all the benefits and types this is the best option for people who are planning retirement savings.